Photonics West industry update paints a positive outlook. Matthew Dale reports

Photonics was healthy and growing going into the pandemic, and is appearing to emerge relatively unscathed, with capacity having substantially returned to near-normal levels overall.

So said Stephen Anderson, director of industry development at SPIE, at the recent Photonics West digital forum in March.

‘Many photonics firms managed to escape the worst of the pandemic’s effects, in large part because a large number of the photonics manufacturing entities were classified as essential for national security,’ he said.

While the industry is certainly not back where it would have been had it stayed on the pre-pandemic trajectory, according to Anderson, it is doing well, considering the many hurdles created by covid.

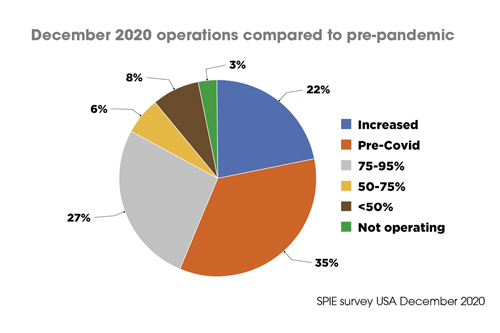

His comments were based on a survey of US photonics firms conducted by SPIE towards the end of 2020 to assess the impact of the pandemic.

Of the 202 firms that took part, 35 per cent claimed to have returned to pre-covid levels of operation, while 22 per cent claimed to have increased in operation.

On the other end of the scale, 8 per cent claimed to be operating at less than 50 per cent capacity, while 3 per cent claimed to not be operating at all.

In between, 27 per cent said they were between 75 to 95 per cent capacity, and 6 per cent were operating between 50 to 75 per cent capacity.

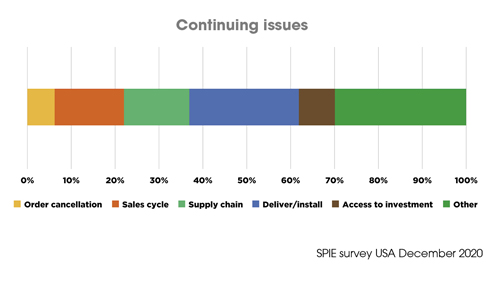

Issues continuing to be faced by photonics firms caused by the pandemic relate mostly to order distribution and access to investment.

Delivery and onsite installation of products has also continued to prove problematic, with about 25 per cent of SPIE’s survey respondents reporting this as an issue. About half of the respondents reported that order flow was either the same or better compared to pre-pandemic levels, with 28 per cent reporting only a modest reduction in orders.

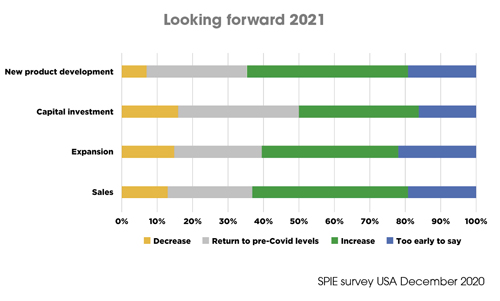

The firms were asked for their expectation of the business environment for December 2021. More than 60 per cent were optimistic, expecting an increase in product development, investment, expansion and sales throughout the year. In addition, 72 per cent of respondents expect staffing levels to either maintain or grow by then. Less than 20 per cent of respondents in any category expected things to get worse.

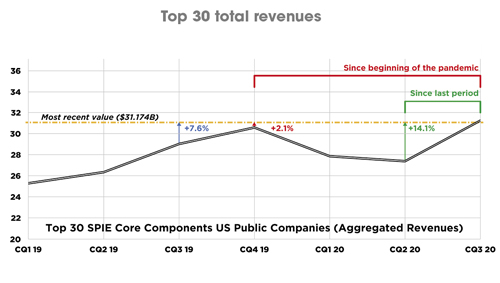

Reinforcing the statement of continuing health for the photonics industry despite the pandemic, Anderson used the aggregated quarterly revenues of the top 30 US firms in SPIE’s core components database, to show that Q3 revenue was up 7.6 per cent in 2020 compared to Q3 2019.

Q3 revenue was also up 14.1 per cent in 2020 compared to Q2, and up 2.1 per cent compared to the largest quarterly revenue (Q4) of 2019.

Aggregated quarterly revenues of the top 30 SPIE photonics core components firms (SPIE Photonics West Industry Update: Trends and Outlook)

Taking stock

Anderson also shared results of SPIE’s biennial report of the photonics components industry, the latest version of which covers 2016-2018 (with 2018-20 data still being prepared).

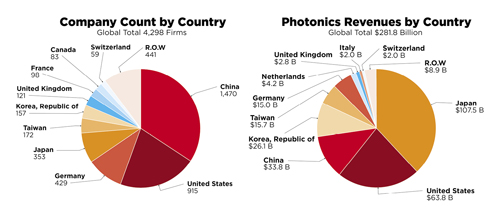

The report states that in 2018, 4,298 firms exhibited photonics components somewhere in the world, a net increase of 530 from 2016. The total number of exhibiting firms has increased at a CAGR of 8 per cent from 2,714 in 2012, when data was first collected for the biennial reports.

China made up the majority of photonics components firms in 2018, while Japan accounted for the most revenue (SPIE Optics & Photonics 2020 Industry Report)

In terms of geographical distribution, in 2018 52 per cent of exhibiting photonics components firms came from Asia, with 24 per cent coming from Europe, 23 per cent from North America and the remaining 1 per cent from the rest of the world. By country, the largest portion of photonics components firms came from China, followed by the US, Germany and Japan. Despite this, Japanese firms accounted for the largest portion of total photonics components revenue, followed by the US. Together they accounted for 61 per cent of total revenue, followed by China, South Korea, Taiwan and Germany. The combined Japanese and US revenue was down from 67 per cent in 2016, which according to Anderson represents the increasing role that China is playing in the photonics components market.

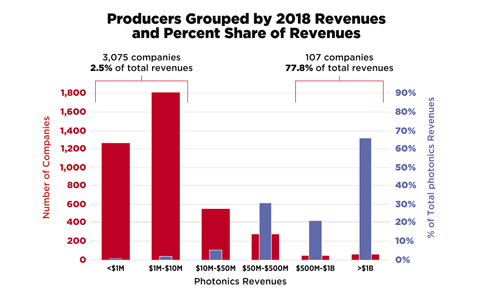

A particularly noteworthy statistic was that while firms with annual revenues below $10m made up the vast majority (3,075) of exhibiting photonics components firms in 2018, these only accounted for 2.5 per cent of total industry revenue. Instead, 77.8 per cent was contributed by just 107 photonics component firms, with each generating annual revenue exceeding $500m. These firms include household names such as Samsung, Huawei, Sony, Canon, Nikon, Ricoh and Corning.

107 firms accounted for 77.8 per cent of photonics revenues in 2018 (SPIE Optics & Photonics 2020 Industry Report )

While in 2012 photonics component industry revenues totalled $182bn, in 2018 they totalled $282bn, representing a CAGR of 7.6 per cent during the six-year period. Of particular note is that Asia has been contributing an increasing portion of the revenue each year, which Anderson reiterated represents the growing footprint of China in the photonics components landscape. The number of jobs in the photonics components industry has increased at a CAGR of 7.8 per cent since 2012, with the number of jobs now exceeding 1 million worldwide: 1,144,000.

Hampered forecasts

It was anticipated by SPIE in December 2019 that the end-user marketplace enabled by photonics components would reach approximately $2.6trn globally in 2020. This was derived from more than 100 photonics-enabled applications.

The 10 major market segments of the enabled marketplace are: semiconductor processing, communications, advanced manufacturing, sensing, lighting, solar, displays, biomedical, defence and consumer.

The CAGR of the combined revenues of these segments was 4.2 per cent between 2012 and 2019.

The consumer market was the largest of the 10 segments by a significant margin, the largest component of which is smartphones.

The top five of these growth segments in 2019 were: biomedical, up 13 per cent thanks to growth in a variety of diagnostics, in addition to food safety testing; defence, up 10 per cent, driven by substantial upswings in video surveillance, perimeter security and sensing, as well as investment in equipment for directed energy systems; sensing, up 10 per cent due to autonomous systems and the Internet of Things continuing to create demand for a wide variety of photonic sensors; advanced manufacturing, up 8 per cent with growth led by lasers for materials processing for applications such as additive manufacturing; and semiconductor processing, up 8 per cent due to healthy revenue growth for optical processing and metrology equipment.

Despite growth across the board, it is now known that for 2019 the total revenues across the enabled marketplace were $2.02trn – somewhat lower than originally anticipated – which makes it unlikely that the forecast $2.6trn figure will be reached for 2020.

‘The pandemic plays a major role in the anticipated 2020 shortfall,’ said Anderson.

Looking beyond photonics, despite the surge in coronavirus cases during the latter part of last year, Anderson said that the US manufacturing sector continues to rebound from the initial shock brought about by the first lockdown.

Using data from the US Census Bureau, he showed that orders for manufactured goods grew sequentially for seven consecutive months in 2020, from May to November. The total value of shipments also increased over seven consecutive months.

Despite this, while the gradual rebound shows noticeable improvement since May 2020, the value of US manufacturers’ has been trailing 2019 levels since the pandemic hit in March.

Anderson reassured that things are headed in the right direction.